Avoid Q4 Tax Penalties Before Year-End | UK Corporations

Prepare Q4 estimated tax payments for UK corporations with deadlines before year-end, as late payments incur up to 5% penalty. See compliance steps now fast.

FINANCE

RUDRA PRAKASH PARIDA

12/5/202517 min read

Q4 Corporate Estimated Tax Payment Calendar with Quarterly Timeline

Table of Contents

Introduction

What Are Fourth Quarter Estimated Tax Payments?

2025 Q4 Estimated Tax Deadlines

Who Must Make Q4 Estimated Payments?

How to Calculate Q4 Estimated Tax Payments

The Four Safe Harbor Methods

Common Q4 Estimated Tax Mistakes

Strategic Q4 Tax Planning

Payment Methods and Documentation

Penalties for Underpayment

Q4 Planning Checklist

Frequently Asked Questions

Take Action Now

Introduction

The fourth quarter estimated tax payment deadline approaches fast and missing it can cost your corporation thousands in penalties and interest.

If your corporation expects to owe $500 or more in federal income tax for the year, the IRS doesn't wait until April to collect. Instead, the tax code requires you to prepay your tax liability throughout the year in four quarterly installments.

For calendar-year corporations, the Q4 deadline is December 15, 2025 just weeks away for those operating on a standard tax year. For fiscal-year corporations, the deadline is the 15th of the 12th month of your tax year.

This comprehensive guide walks you through everything you need to know: exact deadlines, calculation methods, penalty avoidance strategies, and actionable Q4 planning tactics that could save your business significant money.

Why Corporations Must Pay Estimated Taxes

The IRS views estimated tax payments as a way to ensure corporations contribute their share of taxes when they earn income, not months later. This cash-flow mechanism helps the government collect revenue consistently and encourages accurate recordkeeping.

For corporations with significant income fluctuations, this system can feel burdensome. However, safe harbor rules (discussed later) provide flexibility to calculate payments in ways that minimize penalties.

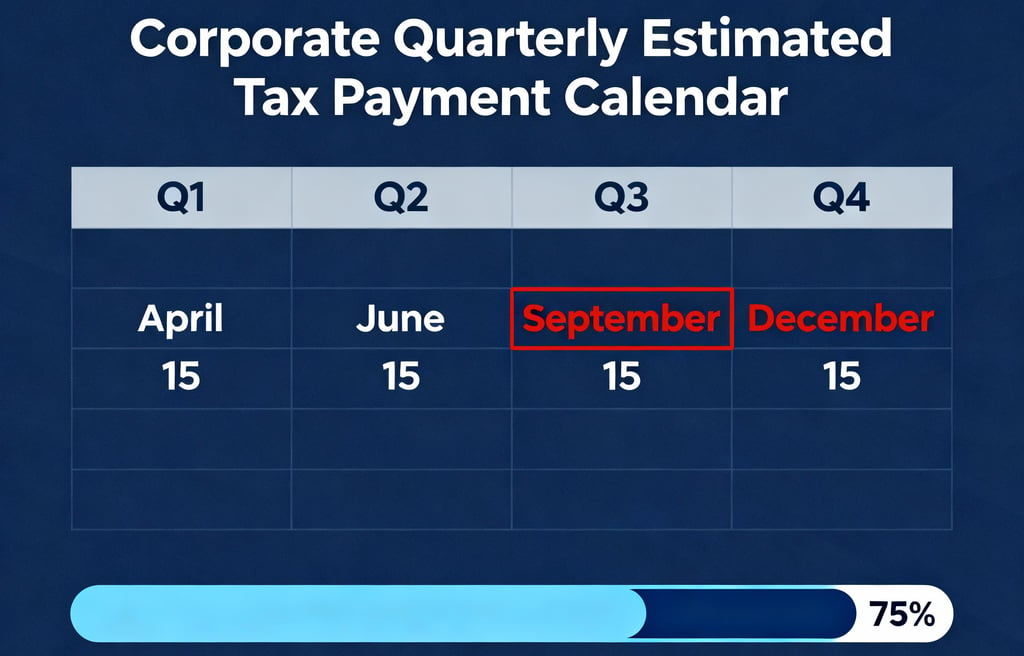

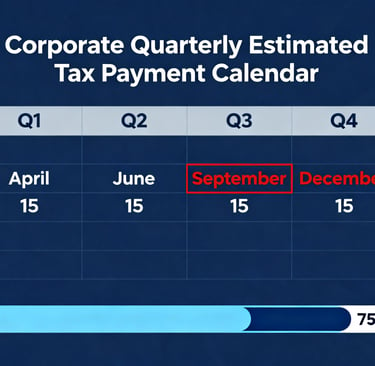

The Four Annual Quarterly Deadlines

Corporations make estimated tax payments on these four dates each calendar year:

Q1 Payment: April 15

Q2 Payment: June 15

Q3 Payment: September 15

Q4 Payment: December 15

For fiscal-year corporations, these dates shift to align with your tax year but maintain the same quarterly spacing.

2025 Q4 Estimated Tax Deadlines

Calendar-Year Corporations

For corporations operating on a standard January 1 – December 31 tax year, the fourth quarter estimated tax payment deadline is December 15, 2025.

This date applies to most U.S. corporations. If December 15 falls on a weekend or holiday, the deadline shifts to the next business day.

Fiscal-Year Corporations

If your corporation operates on a fiscal tax year (for example, July 1 – June 30), your Q4 deadline is the 15th of your 12th fiscal month.

Verify your exact deadline based on your corporation's tax year end. The IRS provides annual tax calendars with specific dates for each scenario.

What Happens If You Miss the Deadline?

The IRS does not grant extensions for estimated tax payments. If you miss the December 15 deadline (or your applicable Q4 date), you'll face underpayment penalties calculated from the original due date even if you pay the amount owed immediately after.

The penalty compounds throughout the missed quarter, making early payment significantly more cost-effective than late payment.

Who Must Make Q4 Estimated Payments?

The $500 Threshold Rule

Your corporation must make Q4 estimated tax payments if it expects to owe $500 or more in federal income tax for the entire tax year (after accounting for credits and withholdings).

If you expect tax liability below $500, estimated payments are optional though not making them costs you nothing as long as your final tax liability remains under that threshold.

Corporations Subject to Estimated Tax Requirements

The following entities must typically make Q4 estimated payments:

C Corporations with expected tax liability exceeding $500

S Corporations and LLCs taxed as corporations if they expect significant tax liability

Closely held corporations and family businesses

Professional corporations and service businesses

Exceptions and Special Situations

Certain corporations may have modified requirements:

Corporations with prior-year tax liability of $0: May not need to make estimated payments if this year's liability will also be near zero

New corporations: Must still make estimated payments if they anticipate owing $500+ in their first tax year

Corporations with significant changes in income: May qualify for annualization methods (discussed later) that adjust quarterly payments to match actual income

How to Calculate Q4 Estimated Tax Payments

Step 1: Estimate Your Total Tax Liability for the Year

Begin by projecting your corporation's total federal income tax liability for 2025.

Calculate this by:

Estimating gross income from all sources (sales, services, investments, etc.)

Deducting ordinary business expenses (salaries, supplies, rent, depreciation, etc.)

Arriving at estimated taxable income

Applying the 21% federal corporate tax rate (the current flat rate for C Corporations)

Subtracting available tax credits (R&D credits, work opportunity credits, etc.)

Example calculation:

Estimated Gross Income: $500,000

Less: Business Deductions: ($150,000)

Estimated Taxable Income: $350,000

Federal Tax Rate × 21%: × 0.21

Estimated Federal Tax: $73,500

Less: Available Credits: ($5,000)

Total Estimated Tax Liability: $68,500

Step 2: Divide by Four for Quarterly Payments

Once you've calculated your total estimated tax liability, divide it equally into four quarterly payments.

Using the example above: $68,500 ÷ 4 = $17,125 per quarter

Each quarterly payment (Q1 through Q4) would be $17,125.

Step 3: Adjust for Prior Quarterly Payments Already Made

By December 15, you'll have already paid Q1, Q2, and Q3 estimates. Your Q4 payment should account for amounts already remitted.

For example:

Total Annual Tax Estimate: $68,500

Divided by 4: $17,125 (per quarter)

Q1 Payment Made: ($17,125)

Q2 Payment Made: ($17,125)

Q3 Payment Made: ($17,125)

Q4 Payment Due (Dec 15): $17,125

If your estimated tax liability has increased during the year, you may need to pay more in Q4 to meet safe harbor requirements.

Using Form 1120-W for Structured Calculations

The IRS Form 1120-W (Estimated Tax for Corporations) provides a detailed worksheet to guide your calculations.

Key sections of Form 1120-W include:

Part I: Expected taxable income for the tax year

Part II: Tax computation using the 21% corporate rate

Part III: Tax credits and adjustments

Part IV: Alternative Minimum Tax (if applicable)

Part V: Quarterly payment schedule

Using Form 1120-W ensures you capture all deductions and credits eligible for inclusion in your estimate, reducing the risk of underpayment penalties.

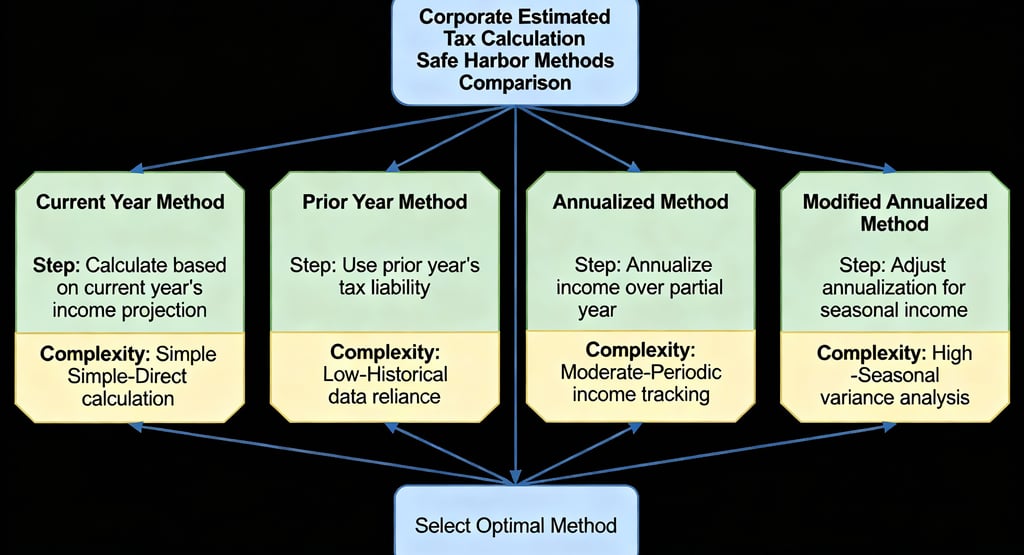

The Four Safe Harbor Methods

The IRS provides four distinct methods for calculating estimated tax payments to avoid underpayment penalties. Your corporation can use whichever method results in the lowest payment requirement.

Understanding these methods gives you flexibility to structure your payments strategically.

Method 1: The Current Year Method (100% of Current Tax)

Under this method, you calculate 25% of your current year's estimated tax for each quarterly payment.

This approach works well for:

New corporations or startup ventures

Businesses expecting significant growth

Companies with substantially increased income compared to last year

Calculation:

Step 1: Estimate current year's total tax liability

Step 2: Multiply by 100% to get total estimated tax

Step 3: Divide by 4 to determine quarterly payment

Step 4: Pay 25% of current year tax each quarter

Example: If you estimate $100,000 in federal tax for 2025, you'd pay $25,000 each quarter under the current year method.

Advantage: Aligns payments with actual current-year income, avoiding overpayment if income has declined.

Limitation: Requires more frequent recalculation if your income projections change throughout the year.

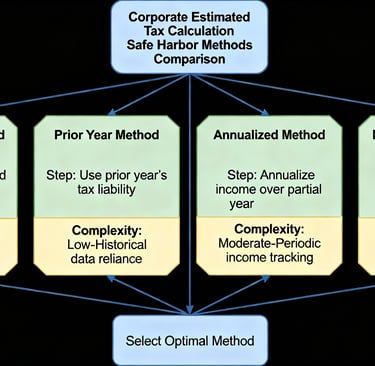

Method 2: The Prior Year Method (Safe Harbor 100% or 110% of Prior Year Tax)

This is the most commonly used safe harbor method. You base your quarterly payments on your prior year's actual tax liability.

The rules are straightforward:

Pay 100% of last year's tax if your prior-year adjusted gross income was $150,000 or less

Pay 110% of last year's tax if your prior-year adjusted gross income exceeded $150,000

Calculation:

Step 1: Identify your 2024 actual tax liability (from your 2024 return)

Step 2: Multiply by 100% (or 110% if AGI exceeded $150,000)

Step 3: Divide by 4

Step 4: Pay that amount each quarter

Example: If your 2024 tax was $80,000 and AGI was $180,000, you'd pay 110% of $80,000 = $88,000 ÷ 4 = $22,000 each quarter.

Advantage: This method is a guaranteed safe harbor if you pay the required amount, you'll avoid underpayment penalties regardless of how your current-year income changes.

Why This Works: Even if 2025 taxes are higher than 2024, you won't face penalties as long as you've paid 100%–110% of last year's amount.

Best for: Stable businesses with predictable, consistent income; corporations wanting to eliminate uncertainty about penalty exposure.

Method 3: The Annualized Income Method

This method bases quarterly payments on actual income earned through each quarter, adjusted as if that income will continue at the same rate through year-end.

This method is ideal for corporations with highly variable or seasonal income.

How It Works:

Q1 Payment: Based on January–March actual income, annualized

Q2 Payment: Based on January–June actual income, annualized

Q3 Payment: Based on January–September actual income, annualized

Q4 Payment: Based on full-year actual income

Calculation Example:

Q1 (through March 31):

- Actual income earned Jan-Mar: $50,000

- Annualized: $50,000 ÷ 3 months × 12 months = $200,000

- Tax at 21%: $42,000

- Q1 payment: $42,000 ÷ 4 = $10,500

Q2 (through June 30):

- Actual income earned Jan-Jun: $140,000

- Annualized: $140,000 ÷ 6 months × 12 months = $280,000

- Tax at 21%: $58,800

- Cumulative payment needed: $58,800 ÷ 4 = $14,700

- Less Q1 paid: $10,500

- Q2 payment: $4,200

Advantage: Minimizes overpayment for corporations with strong Q1-Q2 performance but weaker later quarters (or vice versa).

Limitation: Requires detailed quarterly accounting records and more complex calculations. Most small to mid-size corporations use simpler methods.

Method 4: The Modified Annualized Income Method (IRS-Approved Variation)

A variation of the annualized method allows corporations to base certain quarters on a different income calculation approach, often reducing early-year payment obligations.

When to Use: If your business is highly seasonal or experienced significant income changes during the year, consult a tax professional about this method.

Common Q4 Estimated Tax Mistakes

Mistake 1: Underestimating Annual Income

The Problem: Many business owners project conservative (lower) income estimates, hoping to minimize tax obligations.

In reality, this strategy guarantees an underpayment penalty when actual income exceeds estimates.

The IRS Perspective: Underpayment is underpayment, regardless of intent. The penalty applies automatically if your total estimated payments fall short of safe harbor thresholds.

Better Approach:

Base estimates on actual year-to-date income, adjusted for seasonal trends

If revenue is growing, factor in realistic growth rates rather than assuming flat performance

Update quarterly estimates if income significantly exceeds or falls below earlier projections

When in doubt, estimate higher overpayment generates refunds; underpayment generates penalties

Mistake 2: Forgetting Prior Quarterly Payments

The Problem: Corporation owners sometimes lose track of Q1, Q2, and Q3 payments already made, resulting in duplicate or excessive Q4 payments.

Alternatively, they might fail to account for prior payments and believe Q4 needs to include the full annual amount.

The Fix:

Maintain a payment record with dates and amounts for Q1–Q3

Calculate Q4 as: (Total Annual Tax) – (Q1 + Q2 + Q3 payments already made)

Consider using the IRS EFTPS (Electronic Federal Tax Payment System) to track all payments in one place

Mistake 3: Not Keeping Accurate Financial Records

The Problem: Without real-time financial records, you're essentially guessing at income and deductions.

Inaccurate estimates lead to underpayment penalties and scrambling when filing your return in April.

The Fix:

Implement consistent bookkeeping practices (monthly reconciliation minimum)

Use accounting software to track income and expenses in real-time

Review your financial position quarterly before each estimated tax deadline

Consult with a CPA or bookkeeper to ensure all deductions are captured

Mistake 4: Ignoring Tax Credits You've Earned

The Problem: Many corporations overlook available tax credits (R&D, work opportunity, employee retention, etc.), resulting in overstated estimated payments.

Common Overlooked Credits:

Research & Development (R&D) Credit: Available if your company conducts qualifying research activities

Work Opportunity Tax Credit (WOTC): For hiring from targeted groups

Employee Retention Credit (ERC): Potentially available for certain situations post-pandemic

Energy Efficiency Credits: For capital investments in renewable energy or efficiency

The Fix:

Review your eligibility for all available credits at the start of Q4

If you qualify for substantial credits, adjust Q4 payments downward (following safe harbor rules)

Engage a tax professional to identify credits you might otherwise miss

Mistake 5: Missing the December 15 Deadline

The Problem: Procrastination is costly. Missing the December 15 deadline triggers immediate penalty and interest charges.

Unlike income tax returns, the IRS grants no extensions for estimated tax payments.

The Fix:

Calendar the deadline immediately (not just December 15, but also note it for weekly reminders starting December 1)

Set up automatic payments through EFTPS or your bank days in advance

If approaching year-end, contact your accountant by December 1 at the latest

Strategic Q4 Tax Planning

Q4 Planning Priority #1: Accelerate Deductible Expenses

By December 31, pay or accrue deductible business expenses you've incurred but haven't yet paid.

Timing considerations:

Paid expenses: If you're an accrual-basis corporation, paying bonuses, professional fees, or supplies before year-end creates immediate deductions

Accrued expenses: If your company uses accrual accounting, accruing December expenses (even if not paid until January) creates 2025 deductions

Depreciation adjustments: Consider Section 179 expensing or bonus depreciation for equipment purchases

Potential tax-timing moves:

Bonus payments to employees: Accrue bonuses in Q4, payable in January this creates 2025 deductions if accrual accounting is properly applied

Professional services: Pay accountants, attorneys, and consultants for year-end work by December 31

Equipment and technology: If considering purchases, evaluate whether Section 179 or bonus depreciation options accelerate deductions.

Read more https://growthanalytica.co.uk/year-end-tax-decisions-save-money

Q4 Planning Priority #2: Harvest Tax Losses on Investments

If your corporation holds investments with unrealized losses, consider realizing those losses to offset income.

Example scenario:

- Investment A (stock): Cost basis $20,000, current value $15,000

- Unrealized loss: $5,000

- By selling before year-end, you realize a $5,000 capital loss

- That loss offsets capital gains or ordinary income (up to $3,000/year), reducing 2025 tax

Important: After selling a losing investment, wait at least 31 days before repurchasing the same or substantially identical security (the "wash sale rule"), or your loss is disallowed.

Q4 Planning Priority #3: Review and Adjust Projected Year-End Taxable Income

By December 1, you should have 11 months of actual 2025 financial results. This is your opportunity to verify your estimated tax payments are on track.

Steps:

Calculate actual year-to-date taxable income

Compare to your initial estimate

Determine expected taxable income for December

Calculate total projected 2025 tax liability

Verify you've paid enough to meet safe harbor thresholds

If you've significantly underpaid: Make an additional Q4 payment now.

If you've substantially overpaid: Adjust Q4 payment downward, though confirm this won't jeopardize safe harbor compliance.

Q4 Planning Priority #4: Consider Timing of Major Revenue or Expenses

For accrual-basis corporations, the timing of revenue recognition and expense accrual can affect 2025 vs. 2026 tax liability.

Strategic considerations:

Large contracts due in December/January: Accrual-basis corporations recognize revenue when earned, not when cash is received. If a December contract is substantially complete, it's 2025 revenue even if invoiced in January.

Year-end purchases: Capital purchases create depreciation deductions over time; decide whether 2025 is the optimal year for acquisition

Accrual of December expenses: Ensure December vendor invoices, supplies, and services are properly accrued to 2025

Q4 Planning Priority #5: Plan for 2026 Estimated Taxes

As you calculate Q4 2025 payments, start thinking about 2025 actual tax liability and how it affects 2026 estimated payments.

Remember: 2026 Q1 payments (due April 15, 2026) will be calculated using either:

100% of 2025 actual tax, or

110% of 2025 actual tax (if AGI exceeds $150,000)

If your 2025 tax is substantially higher than 2024, your 2026 Q1 payment will also increase. Planning now prevents Q1 2026 cash-flow surprises.

Payment Methods and Documentation

How to Submit Your Q4 Estimated Tax Payment

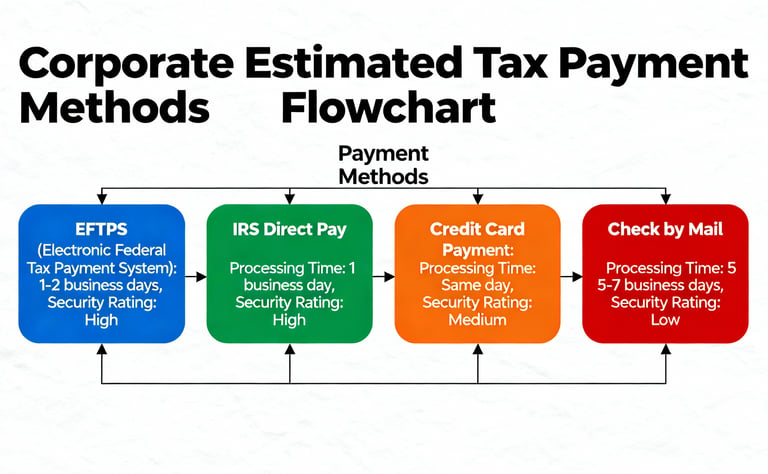

The IRS accepts estimated tax payments through multiple channels:

Method 1: EFTPS (Electronic Federal Tax Payment System)

EFTPS is the IRS-preferred payment method it's free, secure, and provides real-time confirmation.

Steps:

Enroll at www.eftps.gov

Create your account using your EIN and corporate details

Schedule your December 15 payment at least one business day in advance

EFTPS confirms receipt immediately

Print your confirmation for your records

Advantage: Eliminates mailing delays and provides immediate proof of payment.

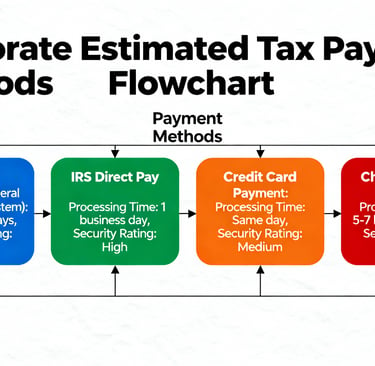

Method 2: IRS Direct Pay

The IRS's online payment portal allows corporations to pay directly without creating an EFTPS account.

Steps:

Visit www.irs.gov/payments

Select "Business Estimated Tax Payment"

Enter your EIN, payment amount, and payment type (Form 1120-ES)

Complete the transaction

Receive an immediate confirmation

Method 3: Credit or Debit Card (Third-Party Processors)

If you prefer card payments, authorized IRS processors accept Visa, Mastercard, American Express, and Discover.

Payment processors charge a convenience fee (typically 1–2.5% of the payment amount).

Processors include:

Authorize.net

Link

Pay1040

Method 4: Check Payment by Mail

Corporations can mail estimated tax payments by check, though this method carries postmark risk.

Payment details:

Use a check made payable to "United States Treasury"

Include your EIN and "2025 Form 1120-ES" on the memo line

Mail to your appropriate IRS address (varies by state)

Allow extra time for postal delivery ideally mail by December 10 to ensure December 15 receipt

Caution: If your check arrives after December 15, you'll face penalties regardless of the postmark date.

Payment Documentation and Record-Keeping

Maintain detailed records of your Q4 (and all quarterly) estimated tax payments:

Records to Keep:

EFTPS or payment confirmation number

Date of payment and amount submitted

Payment method (check, EFTPS, card, etc.)

Corresponding quarter and tax year (e.g., "2025 Q4")

Any adjustment or amended payment if calculated incorrectly

Where to Store Records:

Corporate tax files (keep copies for at least 3-7 years)

Accounting software (QuickBooks, Xero, etc.)

Cloud-based backup (separate from physical records)

Why This Matters: If the IRS questions your payment record, documentation proves you paid by the deadline and protects against additional penalty claims.

Penalties for Underpayment

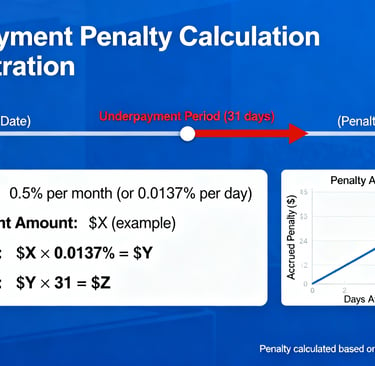

How Underpayment Penalties Are Calculated

If your corporation underpays estimated taxes, the IRS assesses an underpayment penalty separate from any interest charges.

The penalty is calculated per quarter:

Penalty = Unpaid Tax × Federal Interest Rate × (Number of Days Unpaid ÷ 365)

The federal interest rate adjusts quarterly and is based on the IRS's short-term interest rate plus 3%.

Current Penalty Rates for 2025

As of 2025, the federal short-term interest rate is variable. Corporations should expect:

Estimated penalty rate: 8-10% (varies quarterly based on IRS adjustments)

Non-deductible: Unlike interest, underpayment penalties cannot be deducted as a business expense

Compounds by quarter: Each unpaid quarter accrues penalties independently

Example Calculation:

Q4 Required Payment (Safe Harbor): $20,000

Q4 Actual Payment: $15,000

Underpayment: $5,000

IRS Interest Rate (assume 9% quarterly):

$5,000 × 9% × (46 days ÷ 365) ≈ $57

Plus: Underpayment Penalty (assume 8%):

$5,000 × 8% ≈ $400

Total Q4 Cost: $457 in penalties + interest

Note: This example is simplified. Actual calculations involve daily accrual and the precise IRS interest rate for each quarter.

Why Safe Harbor Compliance Saves Money

The critical takeaway: Safe harbor compliance eliminates underpayment penalties entirely.

Even if your actual 2025 tax is $150,000 but you've paid only 110% of your 2024 tax ($100,000), you'll avoid Q4 penalties because you met the safe harbor threshold.

You'll owe any additional tax due when filing your 2025 return, plus interest on the underpaid amount—but no additional penalties apply.

What Happens If You Miss the Q4 Deadline?

Penalties accrue from December 16, 2025 forward for any missed Q4 payment.

Days 1-30 (Dec 16 - Jan 14): Penalty calculation begins immediately at the applicable quarterly rate

Days 31+: Penalties continue accruing until you pay the missed amount

No grace period: The IRS does not extend estimated tax payment deadlines under any circumstances

Takeaway: Every day you delay Q4 payment beyond December 15 costs more in penalties and interest. If you missed Q4 2025, pay immediately when you discover the miss.

Q4 Planning Checklist

Use this checklist to ensure you're fully prepared for Q4 estimated tax payment compliance:

Financial Preparation

Pull year-to-date (Jan–Nov) financial statements and income records

Calculate estimated December income and expenses

Project total 2025 taxable income

Apply the 21% federal corporate tax rate

Identify and quantify eligible tax credits (R&D, WOTC, etc.)

Determine estimated 2025 federal tax liability (after credits)

Document your safe harbor method (prior year, current year, annualized, or modified annualized)

Payment Preparation

Calculate your required Q4 estimated tax payment amount

Verify Q1, Q2, and Q3 payments were made (pull confirmation records)

Calculate Q4 as: (Total Annual Tax) – (Q1 + Q2 + Q3)

Enroll in EFTPS if not already registered

Schedule your Q4 payment for December 13–14 (to ensure receipt by December 15)

Print/save your payment confirmation for tax records

Strategic Planning

Review Q4 deductible expenses accrue any outstanding items by December 31

Consider tax-loss harvesting on underperforming investments

Evaluate timing of large revenue contracts (accrual vs. cash basis)

Review available tax credits and deductions for accuracy

Consult with your CPA if Q4 income is significantly higher/lower than originally projected

Read More :- https://growthanalytica.co.uk/year-end-corporate-tax-planning-guide-2025

Documentation & Record-Keeping

Store Q4 payment confirmation (EFTPS, Direct Pay, card statement)

Create a summary document: 2025 Quarterly Payment Schedule (all four quarters)

File documentation in your corporate tax folder

Set calendar reminders for Q1 2026 payment (due April 15, 2026)

Post-Payment Follow-Up

Reconcile Q4 payment to your records within 7–10 days

If paid by mail, confirm delivery before December 31

Monitor IRS.gov for any payment discrepancies (check account transcript after 3–4 weeks)

Frequently Asked Questions

Q1: What's the difference between estimated taxes and income tax withholding?

A: Withholding applies to W-2 employees; the employer deducts taxes from paychecks throughout the year. Estimated taxes apply to corporations, self-employed individuals, and businesses without withholding obligations. Both serve the same purpose (prepaying tax) but operate through different mechanisms.

Q2: Can I pay more than the required Q4 estimated amount?

A: Yes, you can overpay. Excess payments (beyond your safe harbor requirement) generate tax credits applied to your 2025 return or refunded to you. Overpayment ensures you won't face underpayment penalties but may tie up cash unnecessarily.

Q3: What if my income declined significantly in 2025 compared to 2024?

A: You have multiple options. The prior-year safe harbor (100–110% of 2024 tax) still protects you from penalties. Alternatively, use the current-year or annualized method to calculate lower payments if current income is substantially lower. Either way, you're protected as long as you comply with one of the four methods.

Q4: Do S-corporations make estimated tax payments?

A: S-corporations themselves don't pay federal income tax; instead, income passes through to shareholders. However, if an S-corporation has self-employment tax or owes federal tax separately (rare), it may need estimated payments. Most S-corp owners, however, make individual estimated payments as shareholders.

Q5: What if I'm unsure about my year-end income projection?

A: If uncertain, use the safer prior-year method: pay 100–110% of your 2024 tax liability in Q4. This eliminates penalty risk while giving you flexibility. When you file your 2025 return, any additional tax due is paid at that time (with interest but no additional penalties).

Q6: Can the IRS grant a waiver for missed Q4 payments?

A: The IRS rarely waives estimated tax payment penalties. "Reasonable cause" defenses exist but are narrowly applied. The best strategy is to avoid missing payments entirely. If you discover a missed payment, pay immediately and consult a tax professional about penalty relief options.

Q7: Do I need to file Form 1120-ES even if I pay electronically?

A: No. Form 1120-ES is a worksheet to help you calculate your payment. You don't file it with the IRS. Once calculated, you submit payment through EFTPS, Direct Pay, or by check. The IRS tracks your payment against your EIN and tax account automatically.

Q8: What if my corporation expects a net operating loss (NOL) in 2025?

A: If you anticipate a net loss, your estimated federal tax may be $0 (or even result in a refund if you've overpaid in prior quarters). You can stop making estimated payments once your year-to-date income indicates a loss. Adjust Q4 payments accordingly and document your reasoning.

Q9: How does bonus depreciation affect Q4 estimated payments?

A: Section 179 expensing and bonus depreciation create immediate deductions for qualifying asset purchases, reducing 2025 taxable income and thus lowering estimated taxes. If you purchase qualifying equipment in Q4, update your year-end projection to capture the deduction in 2025, which may reduce your Q4 payment requirement.

Q10: Can I pay Q4 early (before December 15)?

A: Yes, you can pay Q4 as soon as you've calculated it (even in September or October). Early payment satisfies the safe harbor requirement and reduces your end-of-year stress. However, early payment doesn't create additional credits or benefits—it simply fulfills your obligation sooner.

Key Takeaways

✅ Calendar-year corporations must pay Q4 estimated tax by December 15, 2025 (or the 15th day of the 12th month for fiscal-year corporations).

✅ Corporations owing $500+ in annual tax must make quarterly estimated payments to avoid penalties.

✅ The prior-year safe harbor (100–110% of 2024 tax) is the simplest, most secure method for most corporations.

✅ Underpayment penalties currently run 8–10% annually and are non-deductible—making compliance far cheaper than noncompliance.

✅ EFTPS is the fastest, most secure payment method; pay by December 13–14 to ensure timely receipt.

✅ Strategic Q4 tax planning—accelerating deductions, harvesting losses, and projecting year-end income—can significantly reduce your overall 2025 tax burden.

Take Action Now

The Q4 estimated tax deadline is weeks away. Don't let procrastination turn a simple compliance task into a costly penalty.

Here's your immediate action plan:

This Week

Calculate your projected 2025 total tax liability using Form 1120-W or your accounting software

Verify Q1–Q3 payments were made and document amounts

Determine your Q4 payment amount using your chosen safe harbor method

Next Week

Enroll in EFTPS if you haven't already (takes 15 minutes)

Schedule your Q4 payment for December 13–14

Consult your CPA if year-to-date income is significantly different from your original projection

Before December 15

Execute your Q4 payment via EFTPS, Direct Pay, or approved card processor

Print and file your payment confirmation with your corporate tax records

Document your safe harbor calculation method for your 2025 tax return preparation

Strategic Next Steps

If you want to maximize your 2025 tax efficiency beyond Q4 compliance:

Review your 2026 estimated tax obligations (now that 2025 is nearly complete, your April 2026 Q1 payment is already calculable)

Schedule a year-end tax strategy session with a CPA to identify additional deductions, credits, or timing opportunities

Implement quarterly bookkeeping reviews in 2026 to avoid Q4 scrambling next year

About the Author

Rudra Prakash Parida

Digital Marketing and Tax Strategy Consultant | Growth Analytics Hub

With expertise in UK and U.S. tax planning, digital marketing strategy, and financial compliance, Rudra has guided dozens of corporations through complex Q4 tax planning and estimated payment requirements. Based in the UK with a focus on multi-jurisdictional business optimization, Rudra combines technical tax knowledge with practical business growth strategies.

Credentials:

Business Analytics Certification

Digital Marketing Strategy Specialist

Published: December 5, 2025

Last Updated: December 5, 2025

Let's Help You Master Q4 Tax Compliance

Fourth quarter estimated tax payments don't have to be stressful. With clear deadlines, safe harbor protections, and strategic planning, your corporation can navigate Q4 compliance confidently and efficiently.

Have questions about your specific situation? Reach out through our consulting services, or download our free Q4 Corporate Tax Planning Checklist to walk through calculations step-by-step.

💡 Pro Tip: Subscribe to our newsletter for quarterly tax deadline reminders, updated penalty rates, and strategic planning insights tailored to corporate business owners.

Contact

Reach out for insights and support

Phone

+447768010239

© 2025. All rights reserved.