Self Assessment Penalties: Appeal Your Fine in 3 Steps [2025 UK Guide]

Reduce your HMRC penalty with our proven appeal strategy. Master the 3-step process to challenge late filing fines. Save £100-£900+ with actionable steps.

FINANCE

Rudra Prakash Parida

12/26/202512 min read

Self Assessment Penalties: Appeal Your Fine in 3 Steps [2025 UK Guide]

If you've received a Self Assessment penalty notice from HMRC, your heart probably sank. The thought of paying an unwanted fine feels frustrating especially if you believe you had good reason for missing the deadline. Here's the truth: you don't have to accept that penalty. Thousands of UK taxpayers successfully appeal HMRC penalties every year by following a clear, three-step process that takes just hours to complete.

In 2024-25, over 1.1 million taxpayers missed the January 31st Self Assessment deadline, collectively receiving approximately £110 million in penalties. Many of these penalties could have been reduced or cancelled with a proper appeal. Whether your tax return was late due to illness, technical failures, bereavement, or a genuine misunderstanding, HMRC has a formal process designed to listen to your appeal but you must act within strict deadlines.

This comprehensive guide walks you through the entire appeal process, explains what counts as a "reasonable excuse" in HMRC's eyes, and shows you exactly how to present your case for maximum success. By the end, you'll know precisely what to do when (and if) your appeal is rejected, and how to escalate your case if necessary.

Understanding Self Assessment Penalties: What You're Actually Facing

Before you can successfully appeal a penalty, you need to understand exactly what you're being penalised for. Self Assessment penalties come in two main flavors: late filing penalties and late payment penalties. They're calculated differently, escalate dramatically over time, and both can trigger appeals but the timing matters significantly.

Late Filing Penalties: The £100 Gateway Fine

The moment you miss the January 31st deadline for online Self Assessment returns (or October 31st for paper returns), HMRC automatically issues a £100 fixed penalty. This happens regardless of whether you owe any tax at all. The fixed penalty applies even if your tax bill is paid in full and on time. This is a crucial detail many taxpayers overlook it's not about the amount of tax; it's about the failure to file by the deadline.

If your return remains unfiled beyond three months (May 1st), penalties escalate dramatically. You'll face £10 per day for up to 90 days, which adds up to a maximum of £900 in daily penalties. This means a taxpayer who files four months late could face £100 (fixed) + £900 (daily) = £1,000 in total late filing penalties before any further penalties apply.

At the six-month mark (July 31st), an additional penalty of 5% of the tax due or £300, whichever is greater, is applied. At twelve months (January 31st the following year), this repeats: another 5% of tax or £300. For someone with £10,000 in tax liability, these percentages add up to £1,000 per penalty application.

Late Payment Penalties: The Interest Trap

Separate from filing penalties, if your tax remains unpaid, HMRC charges 5% of the unpaid amount at 30 days, 6 months, and 12 months after the deadline. Even worse, the authority also charges interest at 7.75% annually on any overdue tax the highest rate in over two decades.

This creates a compounding problem: miss both the filing deadline and the payment deadline, and you're facing layered penalties plus escalating interest. This is why immediate action matters the longer you wait, the more your total bill grows.

Step 1: Build Your Case with a Legitimate Reasonable Excuse

The foundational step in any successful appeal is understanding what HMRC considers a "reasonable excuse." There is no statutory definition, which means HMRC assesses each case individually based on whether you took "reasonable care" to meet your obligation despite facing a genuine barrier.

In practical terms, HMRC asks: "Would a reasonable person in the same circumstances have done what you did?" If the answer is yes if you genuinely couldn't meet the deadline despite trying you have grounds for appeal.

What HMRC Actually Accepts as Reasonable Excuse

HMRC provides specific guidance on excuses they commonly accept. Serious illness or hospitalisation, particularly close to the deadline, succeeds regularly because health emergencies legitimately prevent financial tasks. You'll need medical evidence GP notes, hospital discharge letters, or appointment records but HMRC recognises that acute health crises take priority.

Death of a close relative shortly before the deadline is widely accepted. Bereavement affects your mental capacity to manage financial affairs, and HMRC understands this. Documentation should include the death certificate and evidence of the close relationship.

Technical failures genuinely beyond your control can work, but this requires specific evidence. A genuine HMRC website crash documented with screenshots of the error message, or a software provider's documented system failure with timestamped evidence of when it occurred, may succeed. Generic claims like "my computer broke" without dates or supporting evidence fail consistently.

Fire, flood, theft, or other natural disasters that prevent access to documents or the ability to file typically succeed if you can provide police reports, insurance claims, or council records confirming the incident.

Disability-related delays directly linked to your ability to complete a tax return are accepted when documented. This includes physical impairments, mental health conditions preventing focus, neurodivergence affecting organisation, or care responsibilities that created genuine barriers.

The Excuses That Almost Never Work

Understanding what fails is equally important. Simply forgetting the deadline doesn't count as reasonable excuse it suggests carelessness, not a genuine barrier. HMRC gives you over 10 months (200+ working days) to file, so forgetfulness doesn't meet the "reasonable person" test.

Being too busy with work rarely succeeds because you had 10 months to allocate a few hours. General business pressure, while real, doesn't demonstrate that you took reasonable care. Similarly, relying on someone else (accountant, family member, partner) to file without verifying they actually did it is your responsibility, not theirs.

Holiday plans, administrative oversight, and never being told about the deadline all fail consistently. The law assumes adult taxpayers understand their obligations or take steps to learn them.

Gathering Evidence: What Makes Your Case Strong

The difference between a successful appeal and a rejection often comes down to evidence quality. HMRC won't require supporting documents with your initial appeal, but having them ready and being able to produce them quickly if asked dramatically improves your chances.

Create a timeline showing when your barrier occurred and how it prevented you from filing. If you were hospitalised April 15th through May 10th and couldn't possibly file, document those exact dates. If your house flooded three days before the deadline, get evidence of that timing.

Gather supporting documents: medical records, hospital appointment letters, insurance claim documentation, bank statements showing relevant transfers, screenshots of error messages (with timestamps), correspondence with service providers proving they caused the delay.

Write a clear, honest explanation of what happened. Don't exaggerate or invent details HMRC reviews thousands of appeals and recognises embellished claims. Your goal is to show that despite taking reasonable care, a genuine barrier prevented compliance. Honest, detailed explanations with supporting evidence succeed far more often than dramatic narratives without proof.

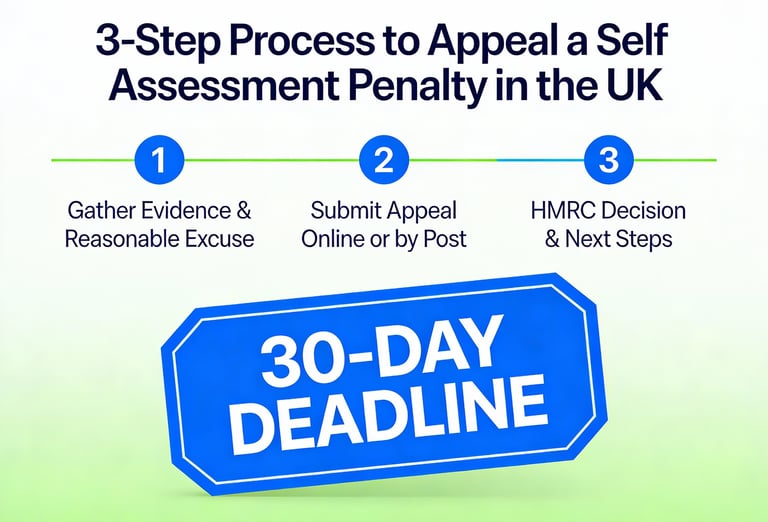

Step 2: Submit Your Appeal Within the Critical 30-Day Window

Timing is everything in the appeal process. You have exactly 30 days from the date on your penalty notice to lodge an appeal and this is a strict deadline. It's not 30 days from when you receive the notice; it's 30 days from the date printed on HMRC's decision notice itself.

This is where most appeals fail before they even start: people simply miss the deadline. The moment you open that penalty notice, mark your calendar for 30 days out. If the deadline falls on a weekend, submit by the preceding Friday.

Option A: Online Appeal (Fastest & Recommended)

The quickest route is submitting your appeal online through your Government Gateway account. This method takes 10-15 minutes and provides instant confirmation.

To access it, log into your HMRC online account and look for the penalty notice in your account. You'll find an "Appeal" button next to the penalty details. Click it and you'll be prompted to enter:

The date the penalty was issued (from your notice)

The date you filed your Self Assessment tax return

Your reasonable excuse and full explanation (write this carefully this is your case)

Any additional context supporting your claim

Upload any supporting documents directly if available (screenshot of error message, hospital letter, etc.). HMRC will provide a confirmation screen immediately showing your appeal was received.

Pro tip: Before you appeal online, ensure your Self Assessment tax return has already been filed. HMRC won't even consider your appeal until the actual return is submitted to them. If you haven't filed yet, do that immediately. The longer the return is outstanding, the more penalty accrues.

Option B: Post Appeal (Traditional but Slower)

If you prefer paper submission, download form SA370 from the HMRC website (or use form SA371 if you're in a partnership). Complete it with:

Your Unique Taxpayer Reference (UTR) number

The penalty issue date and reference

The date you filed your return

Your detailed, honest explanation of your reasonable excuse

Your name, address, and contact details

Attach copies of your supporting evidence (medical records, bank statements, screenshots, etc.). Attach a signed letter providing context if the form doesn't give enough space for your full explanation.

Send everything to:

Self Assessment

HM Revenue and Customs

BX9 1AS

Keep a copy of everything you send. HMRC will respond within approximately 45 days. Written appeals are processed more slowly than online submissions, so submit post appeals as early as possible within the 30-day window.

What If You've Already Missed the 30-Day Deadline?

All isn't lost but your chances decline significantly. You can still appeal, but you must provide a compelling explanation for why your appeal is late. HMRC has discretion to accept late appeals if circumstances justify it (for example, you were hospitalised immediately after receiving the notice and couldn't process it until recovery). However, don't rely on this discretion; submit within 30 days whenever possible.

Step 3: Understand HMRC's Response & Know Your Next Options

What Happens After You Submit Your Appeal

Once HMRC receives your appeal, they assign it to a case officer for review. They typically respond within 45 days, though complex cases sometimes take longer. During this review period, HMRC might request additional information, ask for clarification, or request further evidence.

When HMRC responds, you'll receive a formal letter explaining their decision. There are three possible outcomes.

Outcome 1: Your Appeal Is Accepted (Penalty Cancelled)

If HMRC agrees your explanation constitutes a reasonable excuse, they'll cancel the penalty entirely. If you've already paid the penalty, HMRC will refund the amount plus interest from your payment date. This is the best outcome, and it happens more often than many people realise.

According to HMRC tribunal data from 2023, the authority's success rate in defending penalties across all tribunals was 91.8% which means taxpayers successfully reduced or eliminated approximately 8% of penalties challenged through the tribunal system. At the initial appeal stage with HMRC directly, success rates are moderately higher because HMRC applies reasonable excuse criteria before cases reach tribunal.

Outcome 2: Your Appeal Is Rejected

If HMRC rejects your appeal, you'll receive a letter explaining their reasoning. At this stage, you have two options before escalating to tribunal.

Request an internal review within 30 days of HMRC's decision. This asks a different HMRC officer to reconsider your case. It's not a formal process; you simply send a letter requesting the review and reference your original appeal and penalty reference number. New eyes sometimes spot things the first reviewer missed, and some rejected appeals succeed on review.

If the internal review upholds the rejection, you still have legal recourse: appeal to the First Tier Tribunal.

Outcome 3: Escalation to Tax Tribunal

If you disagree with HMRC's decision even after internal review, you can take your case to the independent First Tier Tribunal. This is a formal legal hearing where both you and HMRC present evidence and arguments before an independent judge.

You have 30 days from HMRC's final decision to request tribunal review. The tribunal will review all evidence afresh and make an independent determination. You can represent yourself, hire an accountant, or engage a tax advisor to present your case.

The tribunal process is more formal than an appeal to HMRC, requiring organized documentation and clear legal arguments. However, it provides genuine independence from HMRC the judge has no bias toward HMRC's position and will rule based solely on whether your reasonable excuse was legitimate.

Important to know: tribunal decisions are binding on both you and HMRC. If the tribunal agrees with you, HMRC must amend or cancel the penalty. If the tribunal agrees with HMRC, you can potentially appeal further to higher courts, but this becomes expensive and requires specific grounds showing the tribunal made an error of law (not simply a different interpretation of facts).

Real-World Examples: Cases That Succeeded

Understanding how real appeals succeeded helps clarify what HMRC actually accepts. While specific taxpayer details remain confidential, certain patterns emerge from published tribunal decisions and guidance.

Case Study 1: Medical Emergency

A self-employed consultant was hospitalised for emergency surgery on January 20th with serious post-operative complications requiring extended bed rest. She was physically unable to sit at a computer or concentrate on financial affairs through mid-February. Her GP provided medical documentation confirming the hospitalisation and recovery timeline. Her appeal succeeded because the medical barrier was genuine, documented, and timed close to the deadline. The penalty was cancelled.

Case Study 2: Technical Failure with Evidence

A taxpayer attempted to file online on January 30th and received an error message from HMRC's portal stating "System temporarily unavailable." He attempted again on January 31st with the same error. He took a screenshot of the error message with the timestamp visible. He filed on February 1st when the system returned to normal. HMRC initially rejected his appeal, claiming the system was available. However, upon internal review, HMRC's technical team confirmed there was a documented outage affecting specific user IDs during that window. The appeal was subsequently accepted because the evidence directly supported his claim.

Case Study 3: Penalty Reduction (Not Full Cancellation)

A taxpayer filed 18 months late due to significant personal circumstances. While her reason was genuine, the extreme lateness meant HMRC couldn't fully cancel the penalty—the rules require minimum penalties even with valid excuses in extreme cases. However, HMRC reduced the penalty from £1,200 to £500 based on her reasonable excuse documentation, saving her £700.

The common thread across successful appeals: specific, documented evidence directly linking the barrier to the inability to file on time.

Frequently Asked Questions About Self Assessment Penalty Appeals

Q: Do I have to pay the penalty while appealing?

A: It's advisable to pay the penalty even while appealing. If your appeal succeeds, you'll receive a refund with interest. If you don't pay and your appeal fails, interest continues accruing on both the penalty and any unpaid tax, making your total bill higher.

Q: What if HMRC asks for more information after I submit my appeal?

A: Provide it promptly. This is normal; HMRC may need clarification or additional evidence. Responding quickly strengthens your case and prevents your appeal from being rejected by default due to lack of cooperation.

Q: If I appeal online, can I add more evidence later?

A: Yes. If HMRC requests additional information, you can provide it. However, the strength of your case is built on your initial submission, so include your best evidence upfront.

Q: How long does the whole process take?

A: Initial HMRC review typically takes 45 days. If rejected and you request internal review, add another 4-8 weeks. Tribunal cases, if necessary, can take 6-12 months depending on the court's workload. The entire process from appeal submission to final tribunal decision can stretch 12-18 months in complex cases.

Q: Can I appeal a late payment penalty using the same process?

A: Yes. The same reasonable excuse criteria, 30-day deadline, and appeal process apply to late payment penalties. However, note that even if your late payment penalty is cancelled, HMRC still charges interest on unpaid tax.

Q: What if I disagree with the tribunal decision?

A: You can appeal to the Upper Tribunal, but only on grounds of legal error (the tribunal misinterpreted the law), not on disagreement with facts. This requires specialist legal representation and is expensive, so it's rare.

Q: Do I need professional help to appeal?

A: Not required, but many people benefit from accountant or tax advisor support. They help organize evidence, frame your reasonable excuse persuasively, and navigate the formal appeal process. For tribunal cases specifically, professional representation significantly improves outcomes.

Key Takeaways: Your Action Plan

1. Act Immediately: Your 30-day appeal window is non-negotiable. From the moment you receive the penalty notice, begin gathering evidence and drafting your appeal.

2. Focus on Reasonable Excuse: Build your entire case around one clear, documented barrier that prevented you from filing. Vague excuses or multiple weak reasons don't work; specific, evidenced reasons do.

3. Submit Online When Possible: The HMRC online portal is fastest and provides instant confirmation. It's your best option unless you lack Government Gateway access.

4. Include Evidence: While HMRC won't require supporting documents upfront, having them ready for quick submission if requested dramatically improves your success chances.

5. Know Your Escalation Path: If HMRC rejects your appeal, request internal review. If that fails, the Tax Tribunal provides genuine independence and your last opportunity before expensive court proceedings.

6. Understand Your Bottom Line: Late filing penalties can reach £1,300+ when combined with daily penalties and percentage-based charges. Late payment penalties add 5% increments plus 7.75% interest. The cost of proper appeal effort (a few hours of your time) is minimal compared to the savings if successful.

Professional Support: When to Get Help

Managing a penalty appeal yourself is absolutely possible if your case is straightforward and evidence is clear. However, consider professional support if:

Your situation involves complex circumstances or multiple contributing factors

You've already missed the 30-day deadline and need persuasive reasoning for late acceptance

Your appeal is rejected and you're considering tribunal escalation

Your tax situation is complex and penalties are substantial (£1,000+)

Accountants and tax advisors specialising in HMRC appeals understand the nuances of what evidence persuades decision-makers. They also ensure procedural requirements are met, reducing the risk of procedural rejection (appeal rejected not on merits, but because forms were incomplete or deadlines missed).

Don't Accept an Unfair Penalty: Take Action Today

Self Assessment penalties are harsh, but they're not final. HMRC has built an appeals process specifically because they recognise that genuine barriers prevent compliance. If you have a legitimate reason for missing your deadline, you stand a real chance of reducing or eliminating that penalty using the three-step process outlined here.

The window for action is tight 30 days from your penalty notice date. The evidence threshold is clear—specific documentation of genuine barriers. The outcome, if successful, is substantial: savings of £100 to £1,300+ depending on your situation.

Start today. Review your penalty notice, gather your evidence, and submit your appeal. Whether you're managing this alone or seeking professional support, the path forward is clear.

Contact

Reach out for insights and support

Phone

+447768010239

© 2025. All rights reserved.